Summary

- The U.S. stock market remains remarkably resilient after a five-year bull market run.

- This does not mean U.S. stocks are not without risks that should be carefully considered.

- One risk more than any other threatens to wreak havoc on stock investor portfolios today.

U.S. stock investors have incredible swagger right now. And why shouldn't they? After all, no matter what gets thrown at the markets over the last several years, stocks end up falling for a few days, at worst, before making up any lost ground and continuing to rally. Recent events have only served to reinforce this confidence, for despite the threat of a cold war revival from the unfolding situation in Ukraine, stocks continue to move persistently higher. It seems nothing can stop the U.S. stock market juggernaut. Unfortunately, it is within this very notion that the greatest danger for investors resides today.

(click to enlarge)

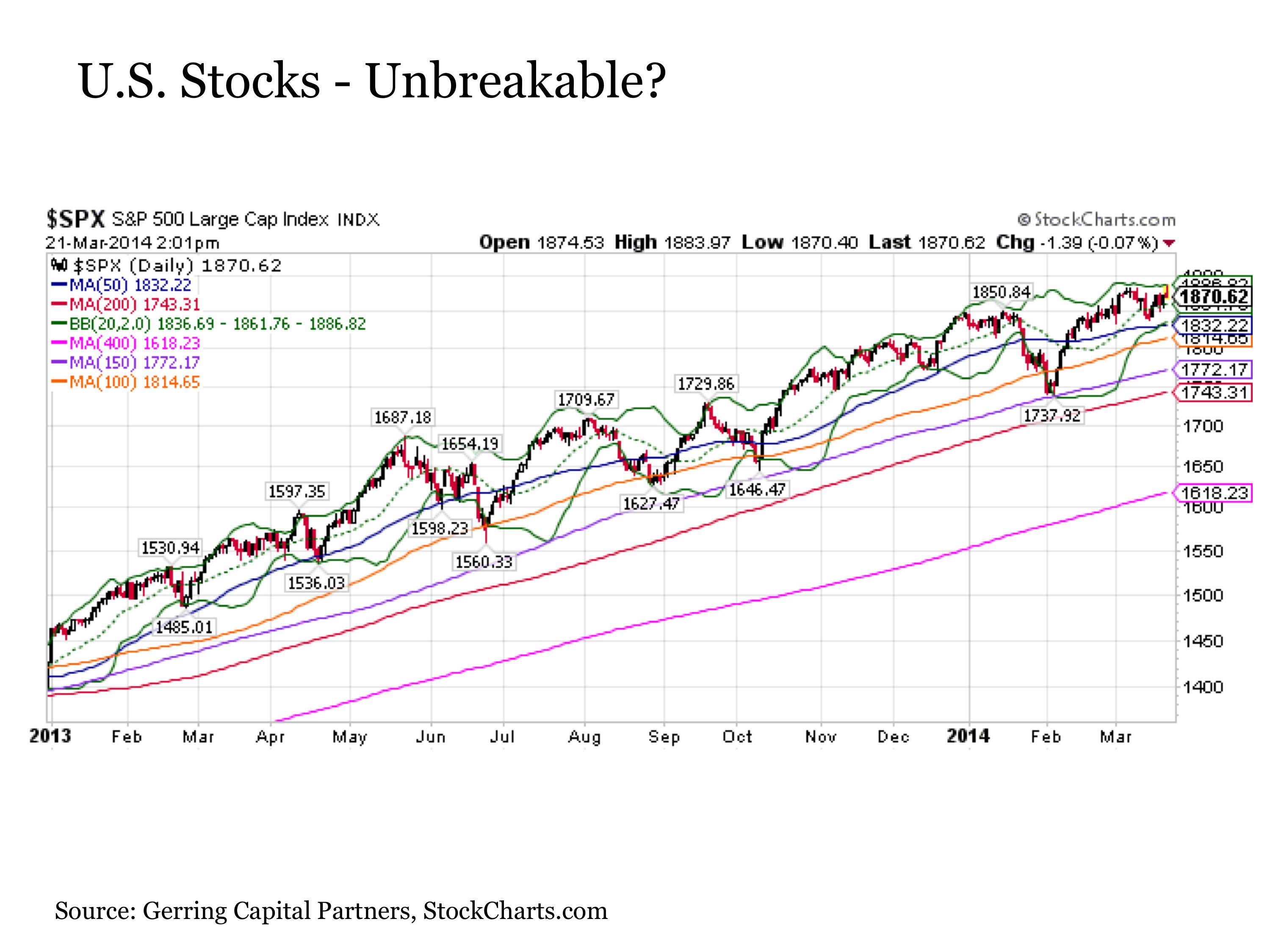

The U.S. stock market's (SPY) sustained and powerful uptrend is impressive, both in its duration and resilience. This is a fact that must be respected from a portfolio allocation standpoint. Now on its sixth year, it ranks as one of the longest bull markets in U.S. history. Moreover, stocks notched their best year during the post-crisis period in 2013, despite generally lackluster economic and corporate fundamentals. And although the stock market is long overdue for even a short-term correction in the 10% to 15% range, the fact that investor sentiment at present is so resoundingly bullish implies that any such dips are likely to be bought, even if they come at the early stages of the next bear market. These are the primary reasons why I remain net long the U.S. stock market at the present time. But this does not mean that I am also not without serious concerns about where the stock market may be headed in the months and years ahead.

(click to enlarge)

In fact, one could easily contend that the U.S. stock market is already showing signs of potential stress as we move through 2014. After all, for all of the talk about the steady rise in stock prices, they are barely positive for the year to date. In addition, three of the primary asset classes that have historically performed well during periods of stock market stress - long-term U.S. Treasuries (TLT), gold (GLD) and volatility (VXX) - are all outperforming stocks so far in 2014. Of course, the stock bulls can easily counter this latter point by highlighting the fact that all three countercyclical asset classes ended 2013 effectively at their lows for the year. Thus, any recent outperformance could simply be explained away by the fact that these are simply oversold bounces, and each is still well behind the path of stocks dating back to the beginning of 2013.

So what, then, is the danger facing the U.S. stock investor today? What could they possibility have to worry about? The greatest threat facing investors today is complacency, for those who have lost sight of risk and the potential havoc it can wreak on their portfolios and long-term financial health face the potential for great discomfort in the end.

The Threat Of Complacency

"Success breeds complacency. Complacency breeds failure. Only the paranoid survive."-- Andy Grove, former CEO, Intel Corporation

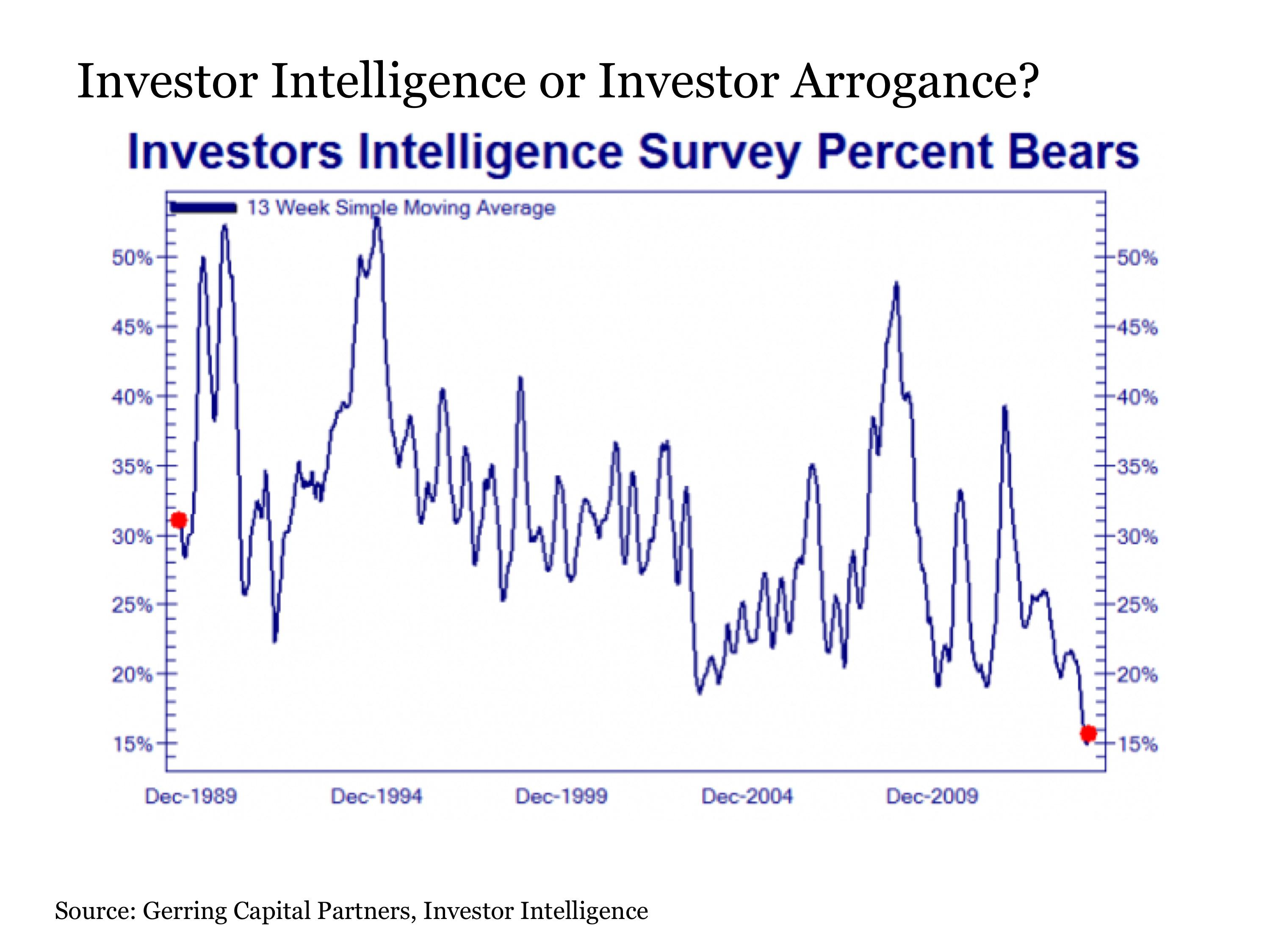

Complacency is a condition that is becoming increasingly widespread the longer today's bull market in stocks rages on. According to Investor Intelligence, the percentage of survey participants who are bearish is currently around 15%, which marks the lowest level in the "Greenspan/Bernanke/Yellen Put" era over the last quarter of a century by 5 percentage points. And this latest surge in investor confidence has come at a time when the economy has stalled, corporate fundamentals have ground to a halt and the geopolitical situation has deteriorated markedly. If one could create a picture of complacency, this would be it.

(click to enlarge)

Does this mean that stock investors should run for cover today? Absolutely not. But at the same time, it also does not mean that they should disregard the signals around them either. For it is usually when investors are most complacent that they are subsequently blindsided by what comes next to steamroll their portfolios.

With this in mind, it is always important from a risk-control perspective to scan the market landscape for potential blind spots that may be obscuring potential trouble ahead. This is particularly true today, with both stock and complacency readings at all-time highs. The following are just a few themes that are worth investor consideration at a time when the typical talking head is repeatedly chirping that stocks are headed nowhere but higher in the months and years ahead.

Stock Market Rehab

The U.S. stock market doesn't seem to know it yet, but it has already been admitted to rehab. Treatment for what, you might ask? To detox the stock market from the steady stream of monetary substances provided by the U.S. Federal Reserve over the last several years. This was a process the Fed tried to get started in 2013, but the timing was poor and the Fed put it off a few months. But then in December, the Fed quietly got the rehab process started by slipping in its first tapering announcement at a time when stocks were on a Christmas-time bender. And it has been cutting stimulus ever since, and will likely continue to wean as long as the U.S. stock market patient continues to cooperate.

So why should investors care? Because post-crisis history has shown that stocks have not fared well once the stimulants wear off.

For example, the S&P 500 Index was trading at 1217 in April 2010, with as reported per share earnings at $60.93 for a P/E ratio of 19.9 when QE1 came to an end. Over the next four months, stocks dropped by as much as -16%, despite the fact that S&P 500 earnings increased by 18% to $71.86 over this same time period. What prevented further declines at the time? The Fed came back to the market with more stimulus in the form of QE2.

The S&P 500 Index was trading at 1345 in July 2011, with as reported per share earnings of $83.87 for a P/E ratio of 16.0 when QE2 drew to a close. Over the next three months, stocks plunged into a mini bear market by falling over -20%, despite the fact that S&P 500 earnings increased by 4% to $86.98 over this same time period. What prevented further declines at the time? The Fed came back to the market with more stimulus in the form of Operation Twist, which managed to keep stocks in a sideways pattern until the launch of QE3 in late 2012.

So where do we stand today? The S&P 500 Index is currently trading at 1872, which represents a 40% increase from the July 2011 levels that were last visited in November 2012. Over this same time period, S&P 500 Index as reported per share earnings have increased by 15% to $100.23, which has resulted in an increase in the P/E ratio to 18.7, which is 16% higher than where it was at the end of QE2. And given that nearly all of the increase in per share earnings has taken place over the last two quarters, it is reasonable to question how much of the latest advance is due to share repurchases and cost-cutting instead of increased demand, given the uneven pace of the economic recovery. Regardless, with the stock market patient scheduled to be fully removed from QE3 narcotics by October, it is reasonable to question how stocks are likely to react this time around. For why exactly will it be different this time? In fact, one would be well served to wonder how the U.S. stock market might react adversely in advance of this ending, particularly given the fact that the second and third-largest world economies in China and Japan, respectively, are also trying to pull off policy withdrawals of their own over the same time frame.

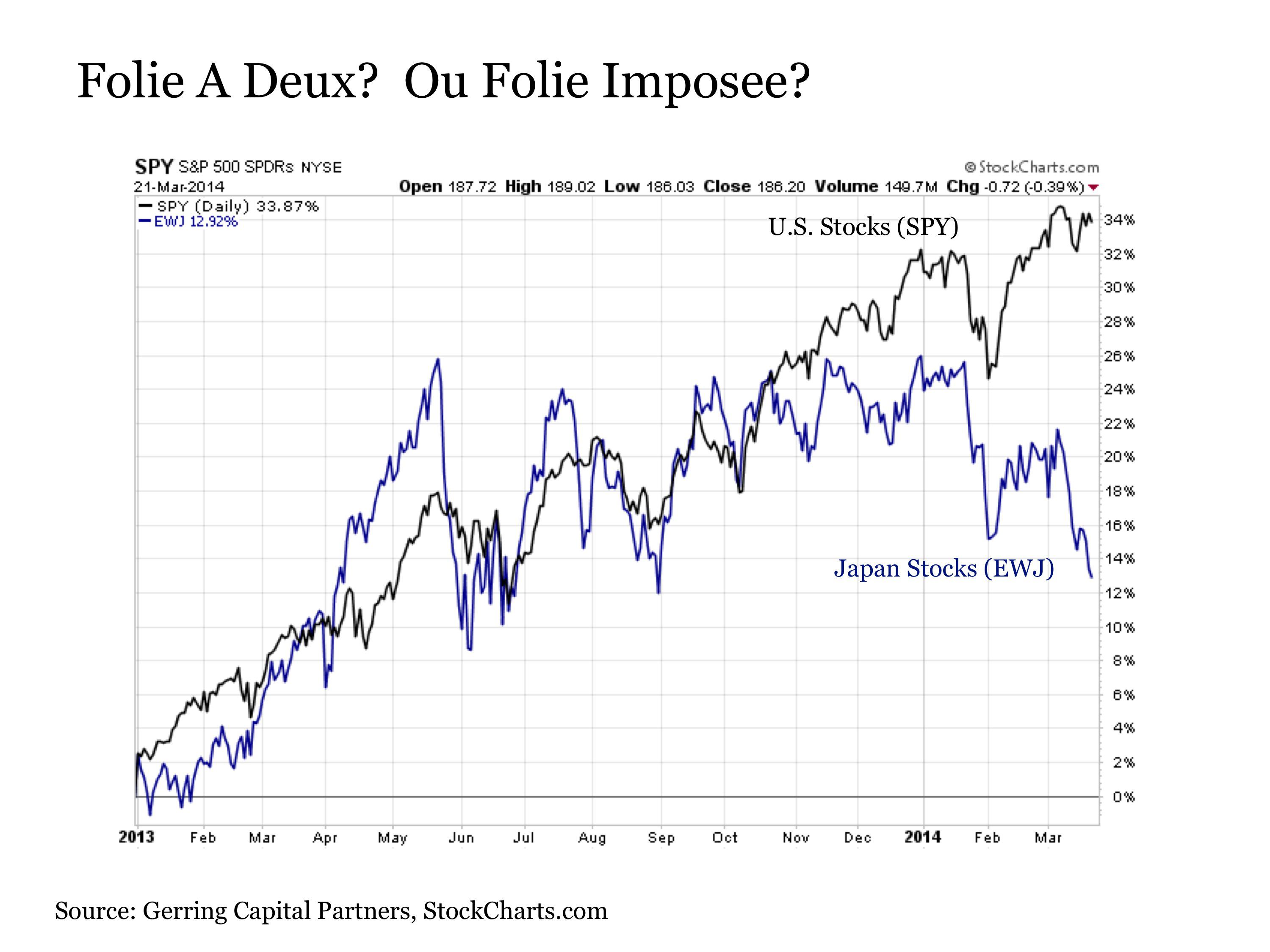

One has to look no further than Japan to see what potentially lies ahead for the U.S. stock market. The U.S. and Japanese economies both entered into massive monetary stimulus programs at around the same time in late 2012 and early 2013. And their stock markets had been moving in lockstep ever since. That is, of course, until recently. For while U.S. stocks remain high as a kite as policy makers work to detox the market from QE3, Japanese stocks (EWJ) seem to have had a more startling return to reality as they progress toward the end of their own planned doubling of the yen (FXY) money supply. In fact, Japanese stocks were never able to reclaim the May 2013 highs achieved not long after the official launch of their stimulus program, neither in currency-unhedged nor currency-hedged (DXJ) terms. And the recent trend for the Japanese stock market since the start of 2014 is far from encouraging, to say the least.

(click to enlarge)

Policy Mistake

"The Fed has been roundly criticized for providing candy to spur markets higher. Consider the challenge when a steady diet of spinach is on offer."--Kevin Warsh, Wall Street Journal Op-Ed, November 12, 2013

The three largest economies in the world are simultaneously drawing to a close massive monetary stimulus programs that have inflated asset prices, including stocks in the United States and Japan, and real estate and commodities prices in China. Unfortunately, hardly anyone complains when asset prices are rising, particularly if they are not feeding through to headline inflation readings (even if it costs dramatically more to fuel your car, stock your fridge and go to college, among other things - many of these price changes are transient, right?). Applying stimulus is the easy part. The hard part is when policy makers either choose or are forced either to remove the application of further stimulus (U.S. and Japan - harder) or take away the stimulus all together (China - hardest).

Such are the risks of a policy mistake increasingly facing the global economy today. The withdrawal of stimulus in order to guide the economic corrective process to a smooth resolution can be painful enough for investo

No comments:

Post a Comment