Investor. Any references to securities are not recommendations or solicitations to buy or sell anything. I may have positions in securities mentioned.

Greed and Capitalism

What kind of society isn't structured on greed? The problem of social organization is how to set up an arrangement under which greed will do the least harm; capitalism is that kind of a system.

Below

are some of our favorite sites. There are hundreds of great sites out

there and we almost certainly missed some fantastic ones so see a name

missing? Feel free to send suggestion to jacob(@)valuewalk.com – Please

only send ‘legit’ and applicable websites – if this is advertising

related see our advertising page – all other emails will be marked as

spam and deleted.

Inside Canada’s Push to Contain the Fallout From Home Capital

by

Josh Wingrove

Finance minister pored over issue before calling big bank CEOs

Regulator steps up vigilance as analysts warn of contagion

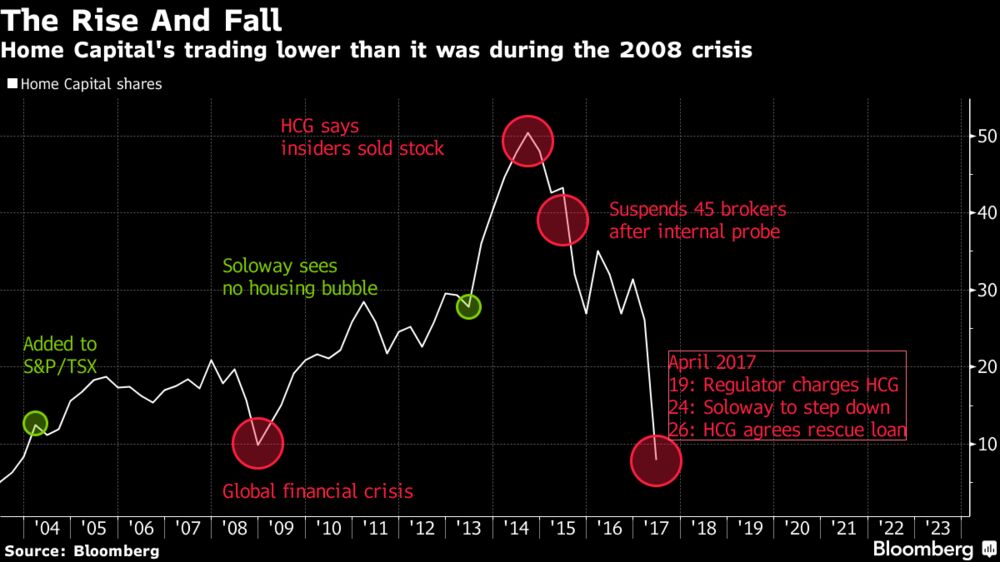

As Home Capital Group Inc.’s shares were in freefall last week, the fight to stop the bleeding at the Canadian mortgage lender had already begun.

It

was late Tuesday night, Ottawa time, when federal Finance Minister Bill

Morneau received his first briefing from department officials just as

he was boarding a plane in Beijing to head home.

Bill Morneau

Photographer: Cole Burston/Bloomberg

Home Capital had been reeling for a week after the Ontario Securities Commission accused the company of misleading investors

over fraudulent mortgages. That was sparking a run on deposits, forcing

the company to take on a C$2 billion ($1.5 billion) emergency credit

line at an effective interest rate of 22.5 percent on funds drawn so

far.

Last Wednesday, with Morneau en route home, Home Capital’s

shares dropped 60 percent by lunchtime as investors bet the onerous

terms of the loan would squeeze the company. There was also contagion

risk. Canada’s major banks saw their shares slump, while Equitable Group Inc., a rival of Home Capital, plunged by almost a third.

Morneau

landed in Ottawa Wednesday night, calling his departmental officials as

he got off the plane for the latest information, according to people

familiar with the discussions. He later spoke with Jeremy Rudin, head of

Canada’s Office of the Superintendent of Financial Institutions, who is

responsible for regulating what the World Economic Forum has called the

“soundest” banking system.

On

Thursday, Morneau’s office pledged his support for Rudin’s OSFI and the

banking sector. “Our government has full confidence” in OSFI to “manage

the situation,” Morneau spokeswoman Annie Donolo said in an email.

The

pledge wasn’t enough to calm investors. While Home Capital’s stock

recovered on Thursday on speculation a buyer for the company might

emerge, the deposit run continued, totaling C$892 million over three

days to close the week. What’s more, the onerous terms of the high-interest lifeline, later revealed by Bloomberg News to be from Healthcare of Ontario Pension Plan, resonated beyond the company.

Run on Deposits

“We

looked and felt, what on earth are they doing?” Equitable Chief

Executive Officer Andrew Moor said in an interview. “We thought that

might cause issues of confidence in the market, frankly, and so

immediately we started reaching out to our bankers.”

Equitable started to face a rash of withdrawals too, losing

about C$75 million daily between Wednesday and Friday -- even though the

Canada Deposit Insurance Corporation provides a safety net by

guaranteeing deposits of up to C$100,000.

OSFI, meanwhile, put out

requests to lenders asking for updates to get a handle on the damage,

though spokeswoman Annik Faucher called it part of “ongoing supervisory

activities.” In a separate statement, she acknowledged the situation has

increased “our level of activity and vigilance.”

Canada’s

alternative lenders, such as Home Capital and Equitable, typically

offer mortgages to borrowers who have trouble getting home loans from

big banks because they lack a credit history, such as the self-employed,

new immigrants and small business owners.

Just as Moor was

reaching out to banks, Morneau was doing the same. On the weekend, he

spoke with heads of the biggest commercial lenders to discuss Home

Capital -- though precisely which bank executives he called isn’t clear.

While Morneau doesn’t consider Home Capital a systemic problem, he was

focused on assessing the risk its woes could spread to other alternative

lenders, according to people familiar with the talks. A core Morneau

message over the past week has been to ensure market stability.

‘System is Working’

By Sunday night, the commercial banks -- including Toronto-Dominion Bank and Bank of Nova Scotia -- agreed to a C$2 billion loan for Equitable at a rate of about 1.6 percent to 1.7 percent.

“Not

many people can go around and borrow C$2 billion off Bay Street in five

days,” said Moor, who said he received commitments from five of

Canada’s six big banks by Sunday night, with the sixth now on side.

It was Monday that Morneau -- a veteran of Toronto’s financial sector -- issued his first public comments.

“Financial

stability and security are the backbone of a strong and resilient

economy,” he said in a statement. “What I’ve seen over the last few days

is proof the system is working as it should.”

The credit line ring-fenced Equitable, which soared by a third on Monday morning, though bank shares continued to slide.

Next Steps

The question now is what to do next with Home

Capital. While it only accounts for 1 percent of Canada’s C$1.4 trillion

mortgage market, it still has almost C$18 billion in mortgages. If

withdrawals continue, it could be unable to renew them or bring in new

business. That could deprive potential home buyers of credit, adding to a

slowdown that’s already showing signs of developing in Toronto and Vancouver.

“This

could be just an isolated situation and that’s the higher-probability

outcome at this point, but you cannot ignore the risk that this can get

messy,” said Aubrey Basdeo, head of Canadian fixed income at BlackRock

Inc. “The focus now is on the potential for a systemic issue across the

economy and it would be folly just to ignore that.”

OSFI

has a four-stage intervention process -- stage four being non-viability

or imminent insolvency. That scenario could include OSFI assuming

temporary control of the institution’s assets, as well as it or CDIC

seeking government approval for a wind-up order. It’s not clear what, if

any, stage Home Capital is at. OSFI and the company declined to

comment.

In some cases, if a company is considered solvent but

illiquid, the Bank of Canada can provide a loan if the affected firm

provides plans for recovery. A spokesman for the central bank declined

to comment.

Home Capital has hired investment bankers for a possible sale, though buyers are scarce --

banks, pensions funds and private equity firms such as J.C. Flowers

& Co. and Fairfax Financial Holdings Ltd. have so far passed. A

piecemeal sale of the mortgage portfolio is another possibility.

Government’s Role

Morneau’s

job may not be done. Though the big banks would have passed on the

customers that took out mortgages with Home Capital, a co-ordinated pick

up of the loans is also an option. The company appointed Alan Hibben to

its board Friday, replacing the outgoing founder.

Some

in the financial industry argue government should take the lead. “It

certainly should be driven by Ottawa, for sure,” said Moor, Equitable’s

chief executive. “They have the resolution authority.”

Morneau has

stressed the importance of market-based solutions. After an effort that

stretched through the weekend, he downplayed any risk Home Capital

could trigger a market correction. “We do not see those two things as

linked,” he said Tuesday in parliament, adding the response so far “is

exactly the way the system should work.”

Direct government

intervention could encourage reckless behavior, Canadian Imperial Bank

of Commerce analyst Robert Sedran wrote in a note to clients. Likewise,

letting a lender fail “would create unnecessary instability in the

housing market, causing fear to mount and potentially spread over to the

banks.”

If current fears are any measure, efforts so far have

worked. Many analysts see Home Capital -- regardless of its ultimate

fate -- as an isolated issue.

“It’s not the beginning of the end,” said Benjamin Tal, deputy chief

economist at CIBC, noting the housing market is instead more vulnerable

to a recession or rising interest rates. “Home Capital is not the

ultimate test.”

Before it's here, it's on the Bloomberg Terminal.LEARN MORE

Billion Dollar Fund Manager Comes Out of Retirement To Bet Against Canadian Real Estate

Short

selling the 'marginal' lenders was what I liked about his approach. It

was 6 months ago that I posted this article. Showing the

patience needed to see an idea to 'fruition' but also how many shadow

lenders are operating in the mortgage market.

10/31/16

Shadow lenders growing in population

By WM

The number of mortgage brokers and non-bank

lenders operating outside of Bank of Canada’s reach is increasing,

including the likes of cash-for-jewelery dealer Harold Gerstel of

Toronto.

Gerstel, 57, owns a cash-for-jewelery shop in the Lawrence Manor

neighbourhood and has found arranging mortgages as another way to earn

dollars.

In his daytime commercial ads, he promises to seal a mortgage in five

business days for low-income borrowers. He adds that these applications

will require little documentation and a record of late payments.

The venture to mortgage broking appears to be fruitful for Gerstel, as

he has sourced hundreds of home loans since 2011 with lightly regulated

non-bank lenders.

“We arrange mortgages for the average Joe,” Gerstel said. “The banks are

very strict today. A lot of these people go to the bank and they get

refused. So they turn to the private market.”

This new industry of mortgage brokers and non-bank lenders is expanding

fast, but the Bank of Canada (BOC) warns homebuyers who deal with less

regulated lenders may come with a hefty risk.

“A sizable proportion of new, uninsured mortgages are being issued to

riskier borrowers,” the BOC report said. “Although less-regulated

lenders account for only a small share of overall lending in Canada,

stress experienced by one or several of these entities could have

adverse financial and economic spillover effects.”

Of all of the mortgages writing in Canada, about 5% come from

unregulated lenders. Eighty-percent of mortgages are created by

federally regulated lenders, including the country’s five biggest banks.

“A lot of this business falls out of the regulated space and into the

shadow banking or unregulated space,” said Martin Reid, president of the

federally regulated non-bank lender Home Capital Group Inc. “It may

become a bigger systemic risk.”

Despite the authorities warning against the likes of him, Gerstel is firm to pursue his second career.

“I’m always going to do a little bit of jewelry but I’d rather do

mortgages because there’s a lot of room for growth there,” he said.

“Every day there’s thousands of thousands of people that need

mortgages.”

Are you looking to invest in property? If you

like, we can get one of our mortgage experts to tell you exactly how

much you can afford to borrow, which is the best mortgage for you or how

much they could save you right now if you have an existing mortgage. Click here to get help choosing the best mortgage rate