Investor. Any references to securities are not recommendations or solicitations to buy or sell anything. I may have positions in securities mentioned.

Greed and Capitalism

What kind of society isn't structured on greed? The problem of social organization is how to set up an arrangement under which greed will do the least harm; capitalism is that kind of a system.

Full Disclosure: Nothing on this

site should ever be considered to be advice, research or an invitation

to buy or sell any securities, please see my Terms +_Conditions page for a full disclaimer.

Paul Tudor Jones Says U.S. Stocks Should ‘Terrify’ Janet Yellen

by

Katherine Burton

and

Katia Porzecanski

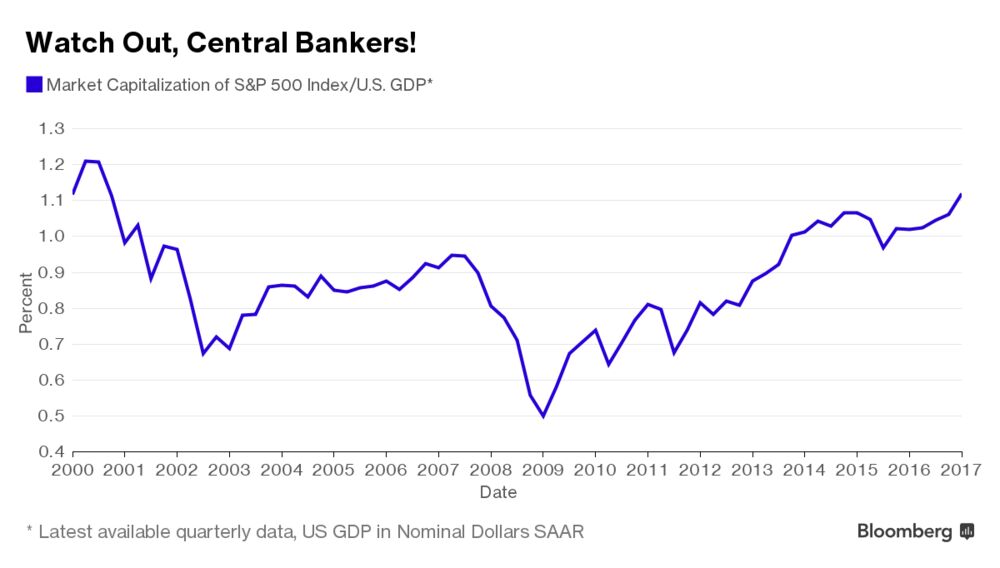

Says U.S. market cap to GDP ratio highest since 2000

Stocks could rise higher after next month’s French election

Guggenheim's Minerd Warns of 'Significant Correction' Billionaire investor Paul Tudor Jones has a message for Janet Yellen and investors: Be very afraid.

The legendary macro trader says that years of low interest rates have bloated stock valuations to a level not seen since 2000, right before the Nasdaq tumbled 75 percent over two-plus years. That measure --the value of the stock market relative to the size of the economy -- should be “terrifying” to a central banker, Jones said earlier this month at a closed-door Goldman Sachs Asset Management conference, according to

people who heard him.

Jones is voicing what many hedge fund and

other money managers are privately warning investors: Stocks are trading

at unsustainable levels. A few traders are more explicit, predicting a

sizable market tumble by the end of the year.

Last week, Guggenheim Partner’s Scott Minerd said he expected

a “significant correction” this summer or early fall. Philip Yang, a

macro manager who has run Willowbridge Associates since 1988, sees a

stock plunge of between 20 and 40 percent, according to people familiar

with his thinking.

Even Larry Fink, whose BlackRock Inc. oversees

$5.4 trillion mostly betting on rising markets, acknowledged this week

that stocks could fall between 5 and 10 percent if corporate earnings

disappoint.

Caution Flags

Their views aren’t widespread. They’ve seen the carnage suffered by a few money managers who have been waving caution flags for awhile now, as the eight-year equity rally marched on.

But

the nervousness feels a bit more urgent now. U.S. stocks sit 2 percent

below the all-time high set on March 1. The S&P 500 index is trading

at about 22 times earnings, the highest multiple in almost a decade,

goosed by a post-election surge.

Managers expecting the worst each

have a pet harbinger of doom. Seth Klarman, who runs the $30 billion

Baupost Group, told investors in a letter last week that corporate

insiders have been heavy sellers of their company shares. To him, that’s

“a sign that those who know their companies the best believe valuations

have become full or excessive.”

Share sales by insiders outstripped purchases by $38 billion in the first quarter, the most since 2013, according to The Washington Service, a provider of data and analysis on insider trading.

Klarman also noted that margin debt -- the money clients borrow from their brokers to purchase shares -- hit a record

$528 billion in February, a signal to some that enthusiasm for stocks

may be overheating. Baupost was a small net seller in the first quarter,

according to the letter.

Another multi-billion-dollar hedge fund

manager, who asked not to be named, said that rising interest rates in

the U.S. mean fewer companies will be able to borrow money to pay

dividends and buy back shares. About 30 percent of the jump in the

S&P 500 between the third quarter of 2009 and the end of last year

was fueled by buybacks, according to data compiled by Bloomberg

Intelligence. The manager says he has been shorting the market,

expecting as much as a 10 percent correction in U.S. equities this year.

China Slowdown

Other

worried investors, like Guggenheim’s Minerd, cite as potential triggers

President Donald Trump’s struggle to enact policies, including a tax

overhaul, as well as geopolitical risks.

Yang’s prediction of a

dive rests on things like a severe slowdown in China or a

greater-than-expected rise in inflation that could lead to bigger rate

hikes, people said. Yang didn’t return calls and emails seeking a

comment.

Even billionaire Leon Cooperman -- long a stock bull --

wrote to investors in his Omega Advisors that he thinks U.S. shares

might stand still until August or September, in part because of flagging

confidence in the so-called Trump reflation trade. But, they’ll eventually resume their climb and end the year moderately higher, he and vice chairman Steven Einhorn wrote in the letter.

When

asked Friday about Jones’s comments, Fed Vice Chairman Stanley Fischer

told CNBC, “There are lots of things that terrify me -- stock market

volatility of the magnitude that we’ve seen for the last couple of years

doesn’t,” without addressing valuations. “Of course we’ll watch very

closely and if we see excess volatility, wonder what is behind it and

whether there are structural features that need fixing or whether it’s

simply recent events or even policy actions.”

Likely Culprit

While Jones, who runs the $10 billion Tudor

Investment hedge fund, is spooked, he says it’s not quite time to short.

He predicts that the Nasdaq, which has already rallied almost 10

percent this year, could edge higher if nationalist candidate Marine Le

Pen loses France’s presidential election next month as expected. Jones

tripled his money in 1987 in large part by correctly calling that

October’s market crash.

While the billionaire didn’t say when a

market turn might come, or what the magnitude of the fall might be, he

did pinpoint a likely culprit.

Just as portfolio insurance caused

the 1987 rout, he says, the new danger zone is the half-trillion dollars

in risk parity funds. These funds aim to systematically spread risk

equally across different asset classes by putting more money in lower

volatility securities and less in those whose prices move more

dramatically.

Because risk-parity funds have been scooping up

equities of late as volatility hit historic lows, some market

participants, Jones included, believe they’ll be forced to dump them

quickly in a stock tumble, exacerbating any decline.

“Risk parity,” Jones told the Goldman audience, “will be the hammer on the downside.”

Before it's here, it's on the Bloomberg Terminal.LEARN MORE

BOSTON— Jack Meyer trounced rivals when he ran Harvard

University’s endowment in the 1990s. But as a hedge-fund manager, he is

struggling. His Convexity Capital Management LP has lost $1 billion of its

clients’ money over the last few years as once reliable options trades

backfired. Investors pulled more than $3.5 billion from the bond shop

last year, its fifth down year in a row. The firm laid off a tenth of

its staff in recent months.

This is one of the most frustrating aspects of the investment

management business. Performance does not persist and strategies, upon

becoming successful, can often start to fail once enough imitators show

up or the market wizens up about someone keeping a big, giant edge to

themselves.

Almost no one has been able to keep their edge in this game

over the years. It’s weird that investors expect this kind of

persistence from hot managers when they have so many examples in the

world outside of finance that demonstrate how unrealistic this sort of

thing is.

Let’s just mention professional athletes, as an example. For obvious

reasons, investing in Kobe or Jeter after 15 years of stellar

performance wouldn’t make any sense to anyone. Why do we think a fund

manager’s track record would be any more relevant?

The best managers have been the most adaptable.

Warren Buffett went

from owning passive stakes in high quality blue chip companies to

acquiring them outright (see Burlington Northern Railroad). Then he

moved on to becoming a private equity partner in the LBOs of others (see

Heinz).

Carl Icahn went from options market guru to activist hedge

fund. But activism got crowded, so now he’s adapted. The new strategy

appears to be making friends with the President of the United States and

pushing for favorable regulatory changes to enhance the value of public

companies he owns (see CVR Energy). Carl and Warren have been finding new edges and opportunities for decades and decades, but they are exceptional.

Not all investors have the capability of adapting their strategies.

Most are more likely to stick to what they’re doing until it stops

working, and then they keep going anyway. You can convince institutional

investors that you’ve made money for that you’re only cyclically

(temporarily) out of favor for a long time before they give up on you,

especially if you’re a name brand.

Even if you do attempt to adapt, there’s no guarantee it will work.

Lots of long-short hedge fund kings have been unable to generate the

type of reliable alpha that has been legislated out of existence by the

onset of Reg FD (Fair Disclosure). It just took a decade or so for this

to become apparent. And in the meantime, their pivots into macro

strategies have been mostly disastrous.

When you’re looking at the performance record of a firm like

Renaissance Technologies, it’s tempting to believe that they’ve built an

unstoppable alpha machine that could run itself, it’s so consistent.

But this is hardly the case. Every day there are hundreds of PhDs and

other assorted geniuses showing up to their cabin in the woods to keep

coming up with new edges. Because the old ones eventually stop working.

There are no alpha machines, there are only tools and systems that may

allow them to find alpha somewhere new.

This is not the sort of enterprise in which thousands of

professionals and organizations will thrive. There simply isn’t enough

room. It’s a small, rarefied world with enormous potential rewards being

chased by millions. Maintaining an edge is unrealistic, but finding new

edges on a regular basis may be even more unrealistic.

Full

Disclosure: Nothing on this site should ever be considered to be

advice, research or an invitation to buy or sell any securities, please

see my Terms & Conditions page for a full disclaimer.

A chat bot that helped overturn 160,000 parking tickets is now giving free legal aid to asylum-seeking refugees through Facebook.

DoNotPay,

which has been dubbed the world’s first robot lawyer, was created by

London-born Stanford University student Joshua Browder.

The

20-year-old, who has made Forbes’ 30 Under 30 list of the brightest

young entrepreneurs, designed his first bot to help people fight parking

fines.

Now the

‘Robin Hood of the internet’ has just expanded the chat bot to Facebook

Messenger to help refugees in the US, Canada and the UK claim asylum.

“Ultimately, I just want to level the playing field so there’s a bot for everything,” he told Business Insider.

“I

originally started with parking tickets and delayed flights and all

sorts of trivial consumer rights issues,” he added. “But then I began to

be approached by these non-profits and lawyers who said the idea of

automating legal services is bigger than just a few parking fines. So

I’ve since tried to expand into doing something more humanitarian.”

The

bot asks users a series of questions in real time, such as “Have you,

your family or colleagues ever experienced harm or threats?”

It

helps refugees seeking asylum in the United States or Canada complete

the necessary forms and those applying in the UK, who will then have to

apply in person, with the support documents.

He

added: “The success of the parking tickets has made me realise this is

bigger than parking charges. I think there’s a real value in providing

free legal help through a chat bot.”

FILE PHOTO: Professional sports gambler William ''Billy'' Walters departs Federal Court after a hearing in Manhattan, New York City, New York, U.S., July 29, 2016. REUTERS/Andrew Kelly/File Photo

U.S. | Fri Apr 7, 2017 | 3:38pm EDT Las Vegas sports gambler Walters convicted of insider trading

Famed Las Vegas sports gambler William "Billy" Walters was convicted on Friday of insider trading charges in a scheme that prosecutors said enabled him to make more than $40 million and involved a stock tip to star professional golfer Phil Mickelson.

In their second day of deliberations, jurors found Walters, 70, guilty on all 10 counts he faced, including securities fraud, wire fraud and conspiracy, following a three-week trial in federal court in Manhattan.

"Today, Billy Walters lost his bet that he could cheat the securities markets and get away with it scot-free," acting U.S. Attorney Joon Kim said in a statement. Walters, who built a fortune as one of the most successful U.S. sports bettors, expressed disbelief to reporters after hearing the six-man, six-woman jury's verdict. "If I had made a bet I would have lost. I just did lose the biggest bet of my life," Walters said. "Frankly I'm in total shock."

Barry Berke, Walters' lawyer, said he would appeal. Walters is scheduled to be sentenced on July 14. Walters was charged in May after a high-profile probe focused on what prosecutors called his scheme to obtain confidential tips about Dean Foods Co from its chairman, Thomas Davis. Prosecutors said that from 2008 to 2014, Walters generated $32 million of profit and avoided $11 million of losses by trading on inside information about Dean Foods from Davis. Walters earned another $1 million trading on a tip about Darden Restaurants Inc, operator of the Olive Garden restaurant chain, they said. Davis, who testified against Walters as part of a plea deal, told jurors he passed tips ahead of Dean Foods' earnings reports and a 2012 spinoff of part of its business, using "burner" phones.

Prosecutors said Walters at one point made a recommendation to Mickelson that the golfer, who at the time owed him a gambling debt, buy Dean Foods stock. Mickelson was not accused of wrongdoing and did not testify at trial, but he reached an agreement with the U.S. Securities and Exchange Commission in2016 to pay back $1.03 million the regulator said he earned trading the dairy company's stock.

At trial, Berke argued Davis had lied to get a sweetheart deal for himself. He contended -

Walters won big as a stock trader the same way he did as a sports gambler - with diligent research and keen instincts.

The case is U.S. v. Davis et al, U.S. District Court, Southern District of New York, No. 16-cr-00338.

(Reporting by Nate Raymond and Brendan Pierson in New York; Editing by Leslie Adler and Lisa Shumaker)