Investor. Any references to securities are not recommendations or solicitations to buy or sell anything. I may have positions in securities mentioned.

Wednesday, November 25, 2015

Alive

Alive

Tuesday, November 24, 2015

How much does it cost to produce a barrell of oil?

It costs $36.20 to produce one barrel of #oil in the U.S. How about the rest of the world? http://cnnmon.ie/1MP7w6K

Monday, November 23, 2015

How Yogi Berra's 'Yogi-isms' Apply to Investing

Oaktree Capital Group co-Chairman Howard Marks discusses how emotion and human nature play into investing. He speaks on "Bloomberg ‹GO›." (Source: Bloomberg)

http://www.bloomberg.com/news/videos/2015-11-20/how-yogi-berra-s-yogi-isms-apply-to-investing

Saturday, November 21, 2015

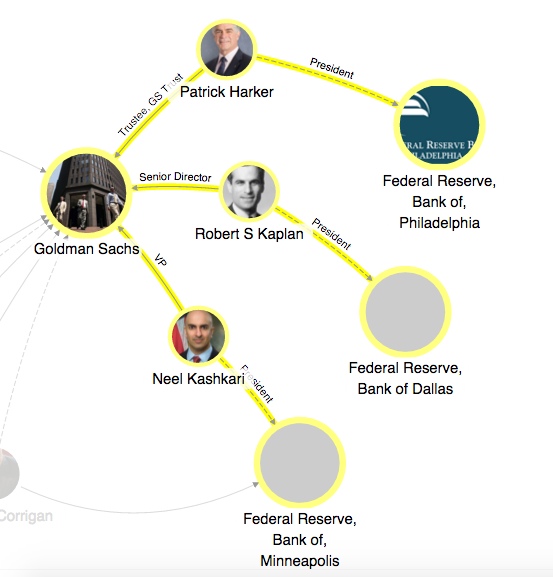

Goldman Sachs/Fed revolving door map.

A new take on our Goldman Sachs/Fed revolving door map.

Take a look: http://littlesis.org/maps/1120-goldman-sachs-alum-run-the-fed …

Russian Ruble

Goldman Sachs advises to buy Russian ruble in 2016

The US investment bank predicts the ruble will be on the list of

good performing currencies next year along with the US dollar and the

Mexican peso, Bloomberg reports.

Goldman Sachs recommends buying Russian and Mexican currencies over South Africa’s rand and Chile’s peso.

This week, the ruble has grown three percent, but seems not strong enough to continue the trend in 2015.

“Ruble assets have found useful support over the last week on a perceived rapprochement between Russia and the West. This relationship may, however, will be tested over the coming days and weeks as fundamentals continue to be weak, oil prices remain under pressure and a December Fed liftoff seems increasingly likely,”

Ivan Tchakarov, economist at Citigroup told Bloomberg.

Goldman Sachs also said the greenback would grow in value in 2016 against the euro and yen. In 2015, the dollar has been growing compared to all of its peers, as the US Federal Reserve gets closer to hiking interest rates and the European Central Bank and Bank of Japan continued monetary stimulus.

Ruble will make 'Made in Russia' a global brand – World Bank economist http://on.rt.com/6vjf

This week, the ruble has grown three percent, but seems not strong enough to continue the trend in 2015.

“Ruble assets have found useful support over the last week on a perceived rapprochement between Russia and the West. This relationship may, however, will be tested over the coming days and weeks as fundamentals continue to be weak, oil prices remain under pressure and a December Fed liftoff seems increasingly likely,”

Ivan Tchakarov, economist at Citigroup told Bloomberg.

Goldman Sachs also said the greenback would grow in value in 2016 against the euro and yen. In 2015, the dollar has been growing compared to all of its peers, as the US Federal Reserve gets closer to hiking interest rates and the European Central Bank and Bank of Japan continued monetary stimulus.

Ruble will make 'Made in Russia' a global brand – World Bank economist http://on.rt.com/6vjf

Ruble will make 'Made in Russia' a global brand – World Bank economist http://on.rt.com/6vjf

Tuesday, November 17, 2015

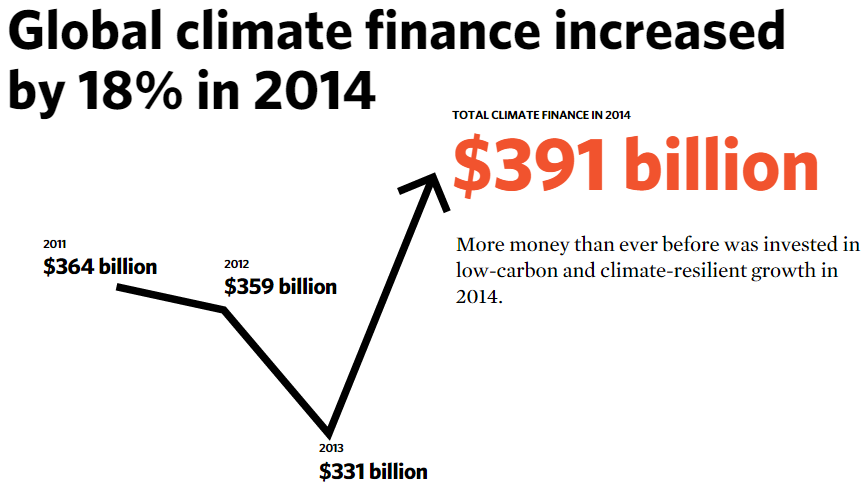

Climate finance rose 18% last year

Climate finance rose 18% last year to reach $391 billion, with $292bn in renewable energy:

Wednesday, November 11, 2015

Financial Secrecy Index

Introduction

| The

Financial Secrecy Index ranks jurisdictions according to their secrecy

and the scale of their offshore finanical activities. A politically

neutral ranking, it is a tool for understanding global financial

secrecy, tax havens or secrecy jurisdictions, and illicit financial

flows or capital flight. The index was launched on November 2, 2015. Shining light into dark places An estimated $21 to $32 trillion of private financial wealth is located, untaxed or lightly taxed, in secrecy jurisdictions around the world. Secrecy jurisdictions - a term we often use as an alternative to the more widely used term tax havens - use secrecy to attract illicit and illegitimate or abusive financial flows. Illicit cross-border financial flows have been estimated at $1-1.6 trillion per year: dwarfing the US$135 billion or so in global foreign aid. Since the 1970s African countries alone have lost over $1 trillion in capital flight, while combined external debts are less than $200 billion. So Africa is a major net creditor to the world - but its assets are in the hands of a wealthy élites, protected by offshore secrecy; while the debts are shouldered by broad African populations. Yet all rich countries suffer too. For example, European countries like Greece, Italy and Portugal have been brought to their partly knees by decades of tax evasion and state looting via offshore secrecy. A global industry has developed involving the world's biggest banks, law practices, accounting firms and specialist providers who design and market secretive offshore structures for their tax- and law-dodging clients. 'Competition' between jurisdictions to provide secrecy facilities has, particularly since the era of financial globalisation really took off in the 1980s, become a central feature of global financial markets. The problems go far beyond tax. In providing secrecy, the offshore world corrupts and distorts markets and investments, shaping them in ways that have nothing to do with efficiency. The secrecy world creates a criminogenic hothouse for multiple evils including fraud, tax cheating, escape from financial regulations, embezzlement, insider dealing, bribery, money laundering, and plenty more. It provides multiple ways for insiders to extract wealth at the expense of societies, creating political impunity and undermining the healthy 'no taxation without representation' bargain that has underpinned the growth of accountable modern nation states. Many poorer countries, deprived of tax and haemorrhaging capital into secrecy jurisdictions, rely on foreign aid handouts. This hurts citizens of rich and poor countries alike. |

| ||||||||||||||||||||||||||||||||||||||

In identifying the most important providers of international financial secrecy, the Financial Secrecy Index reveals that traditional stereotypes of tax havens are misconceived. The world’s most important providers of financial secrecy harbouring looted assets are mostly not small, palm-fringed islands as many suppose, but some of the world’s biggest and wealthiest countries. Rich OECD member countries and their satellites are the main recipients of or conduits for these illicit flows.

The implications for global power politics are clearly enormous, and help explain why for so many years international efforts to crack down on tax havens and financial secrecy were so ineffective, it is the recipients of these gigantic inflows that set the rules of the game.

Yet our analysis also reveals that recently things have genuinely started to improve. The global financial crisis and ensuing economic crisis, combined with recent activism and exposure of these problems by civil society actors and the media, and rising concerns about inequality in many countries, have created a set of political conditions unparalleled in history. The world's politicians have been forced to take notice of tax havens. For the first time since we first created our index in 2009, we can say that something of a sea change is underway.

World leaders are now routinely talking about the scourges of financial secrecy and tax havens, and putting into place new mechanisms to tackle the problem. For the first time the G20 countries have mandated the OECD to put together a new global system of automatic information exchange to help countries find out about the cross-border holdings of their taxpayers and criminals. This scheme is now being rolled out, with first information due to be exchanged in 2017.

Yet of course these schemes are full of loopholes and shortcomings: many countries are planning to pay only lip service to them, if that -- and many are actively seeking ways to undermine progress, with the help of a professional infrastructure of secrecy enablers. The edifice of global financial secrecy has been weakened - but it remains fully alive and hugely destructive. Despite what you may have read in the media, Swiss banking secrecy is far from dead. Without sustained political pressure from millions of people, the momentum could be lost.

The only realistic way to address these problems comprehensively is to tackle them at root: by directly confronting offshore secrecy and the global infrastructure that creates it. A first step towards this goal is to identify as accurately as possible the jurisdictions that make it their business to provide offshore secrecy.

This is what the FSI does. It is the product of years of detailed research by a dedicated team, and there is nothing else like it out there. We also have a set of unique reports outlining detailed offshore histories of the biggest players in the game.

Click here for the full 2015 ranking. For further questions, click here.

Burger Machine That Wants Your Job

Attention Fast Food Strikers: Meet The Burger Machine That Wants Your Job

by ZeroHedge •

By Tyler Durden at ZeroHedge

Today, U.S. fast-food workers will strike across 270 cities in a protest for higher wages and union rights that they hope will catch the attention of candidates in 2016 elections, organizers said.

The walkouts will be followed by protests in 500 cities by low-wage workers in such sectors as fast food and home and child care, a statement by organizers of the Fight for $15 campaign said on Monday.

The protests and strikes are aimed at gaining candidates’ support heading into the 2016 election for a minimum wage of $15 an hour and union rights, it said.

The strikes and protests will include workers from McDonald’s, Wendy’s, Burger King , KFC and other restaurants, the statement said.

And while we sympathize with their demands for higher wages, here is the simple reason why they will be very much futile.

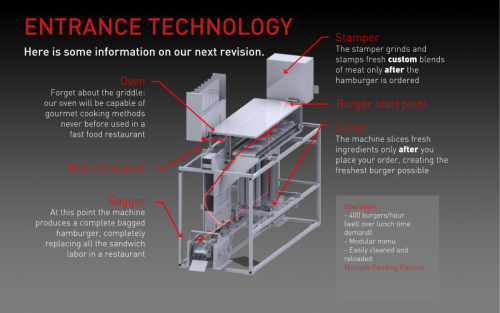

Dear fast food workers of the US – presenting you nemesis: the Momentum Machines burger maker.

According to a recent BofA reported on how robotics will reshape the world, San Francisco start up Momentum Machines are out to fully automate the production of burgers with the aim of replacing a human fast food worker. The machine can shape burgers from ground meat, grill them to order with the specified amount of char, toast buns, add tomatoes, onions, pickles, and finally place it on a conveyor belt.

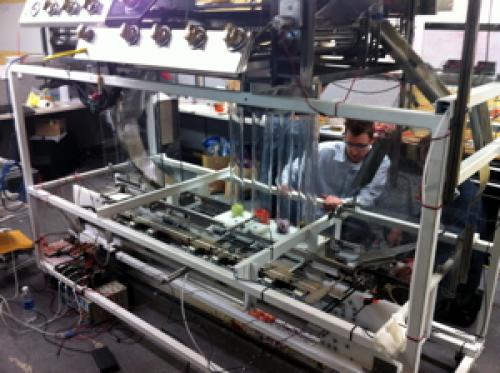

The robot is shown below. It occupies 24 square feet, and is much smaller and efficient than most assembly-line fast-food operations. It provides “gourmet cooking methods never before used in a fast food restaurant” and will deposit the completed burger into a bag. It does all of this without a trace of attitude.

According to public data, the company’s robot can “slice toppings like tomatoes and pickles immediately before it places the slice onto your burger, giving you the freshest burger possible.” Unlike human workers, the robot is “more consistent, more sanitary, and can produce ~360 hamburgers per hour” or a burger every 10 seconds.

Furthermore, future generations of the device “will offer custom meat grinds for every single customer. Want a patty with 1/3 pork and 2/3 bison ground to order? No problem.”

As the company’s website adds, “our various technologies can produce an ever-growing list of common choices like salads, sandwiches, hamburgers, and many other multi-ingredient foods with a gourmet focus.”

But most importantly, it has no wage demands: once one is purchashed it will work with 100% efficiency for years. And it never goes on strike.

As the company’s co-founder Alexandros Vardakostas told Xconomy his “device isn’t meant to make employees more efficient. It’s meant to completely obviate them.”

The company’s philosophy on making millions of fast food workers obsolete:

Finally, for those complaining that there will be no “human touch” left to take the orders, robots have that covered too:

And now it’s time to calculate how many tens if not hundreds of billions in additional welfare spending these soon to be unemployed millions in low-skilled workers will cost US taxpayers.

Source: Dear Striking Fast-Food Workers: Meet the Machine That Just Put You Out Of A Job – ZeroHedge

Today, U.S. fast-food workers will strike across 270 cities in a protest for higher wages and union rights that they hope will catch the attention of candidates in 2016 elections, organizers said.

The walkouts will be followed by protests in 500 cities by low-wage workers in such sectors as fast food and home and child care, a statement by organizers of the Fight for $15 campaign said on Monday.

The protests and strikes are aimed at gaining candidates’ support heading into the 2016 election for a minimum wage of $15 an hour and union rights, it said.

The strikes and protests will include workers from McDonald’s, Wendy’s, Burger King , KFC and other restaurants, the statement said.

And while we sympathize with their demands for higher wages, here is the simple reason why they will be very much futile.

Dear fast food workers of the US – presenting you nemesis: the Momentum Machines burger maker.

According to a recent BofA reported on how robotics will reshape the world, San Francisco start up Momentum Machines are out to fully automate the production of burgers with the aim of replacing a human fast food worker. The machine can shape burgers from ground meat, grill them to order with the specified amount of char, toast buns, add tomatoes, onions, pickles, and finally place it on a conveyor belt.

The robot is shown below. It occupies 24 square feet, and is much smaller and efficient than most assembly-line fast-food operations. It provides “gourmet cooking methods never before used in a fast food restaurant” and will deposit the completed burger into a bag. It does all of this without a trace of attitude.

According to public data, the company’s robot can “slice toppings like tomatoes and pickles immediately before it places the slice onto your burger, giving you the freshest burger possible.” Unlike human workers, the robot is “more consistent, more sanitary, and can produce ~360 hamburgers per hour” or a burger every 10 seconds.

Furthermore, future generations of the device “will offer custom meat grinds for every single customer. Want a patty with 1/3 pork and 2/3 bison ground to order? No problem.”

As the company’s website adds, “our various technologies can produce an ever-growing list of common choices like salads, sandwiches, hamburgers, and many other multi-ingredient foods with a gourmet focus.”

But most importantly, it has no wage demands: once one is purchashed it will work with 100% efficiency for years. And it never goes on strike.

As the company’s co-founder Alexandros Vardakostas told Xconomy his “device isn’t meant to make employees more efficient. It’s meant to completely obviate them.”

The company’s philosophy on making millions of fast food workers obsolete:

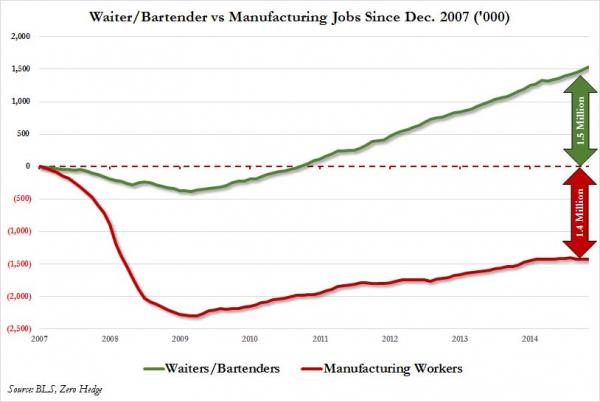

This is a major problem for the US economy, which once built on a manufacturing backbone, has seen the fastest jobs growth in recent years for workers employed by “food service and drinking places” i.e., fast food workers, waiters and bartenders.The issue of machines and job displacement has been around for centuries and economists generally accept that technology like ours actually causes an increase in employment.The three factors that contribute to this are

- the company that makes the robots must hire new employees,

- the restaurant that uses our robots can expand their frontiers of production which requires hiring more people, and

- the general public saves money on the reduced cost of our burgers. This saved money can then be spent on the rest of the economy.

Finally, for those complaining that there will be no “human touch” left to take the orders, robots have that covered too:

And now it’s time to calculate how many tens if not hundreds of billions in additional welfare spending these soon to be unemployed millions in low-skilled workers will cost US taxpayers.

Source: Dear Striking Fast-Food Workers: Meet the Machine That Just Put You Out Of A Job – ZeroHedge

Tuesday, November 10, 2015

The market for cyber-security will be $170 billion by 2020

The Economist @EconBizFin

The market for cyber-security will be $170 billion by 2020

http://econ.st/1HtKlBY

pic.twitter.com/UDncmm8QPi

Liu Yiqian shelled out $170.4 million for Modigliani’s Nu Couché

Did This Chinese Billionaire Rack Up Millions of AmEx Rewards Points Buying That Modigliani?

Imaginechina/AP.

Liu has already established himself as a major buyer of Asian art with a knack for scandalously ostentatious displays of the wealth he amassed investing in the stock market. After paying $36.3 million for a Ming-dynasty ceramic cup at Sotheby’s Hong Kong in July 2014, Liu scandalized the art world when a picture of him gleefully sipping tea from the 500-year-old object once owned by emperors surfaced. If that let-them-eat-cake moment wasn’t enough, Liu also paid for the cup with his American Express card, swiping 24 times and racking up almost 422 million rewards points, according to Bloomberg.

Just a few months later, he paid $45 million for a 15th-century Tibetan tapestry—again with his Centurion. He used his points to fly with his family to New York, where, according to Bloomberg, Liu drew attention for posing for a photo in his underwear in their St. Regis hotel room, assuming the pose of a Tibetan yogi statue he planned to bid for at an upcoming Christie’s New York auction. He won it at a price of $4.9 million.

Courtesy of Christie's.

Liu has not confirmed whether he paid for the Modigliani with his American Express card, but we can only guess what kind of splash he has in store to celebrate

Link: http://www.vanityfair.com/culture/2015/11/modigliani-auction-buyer-amex?mbid=nl_1110_Daily&CNDID=37583177&spMailingID=8239070&spUserID=MTA0NTc2NzY3NjU3S0&spJobID=800995750&spReportId=ODAwOTk1NzUwS0

Related: How Xin Li Went from the Runway to the Center of Nine-Figure Art Auctions

Monday, November 9, 2015

Crude oil rises after OPEC says market to be balanced in 2016

Reuters Top News @Reuters

Crude oil rises after OPEC says market to be balanced in 2016 http://reut.rs/1SELI1O pic.twitter.com/eZwd61QDl7

Monday, November 2, 2015

How Valeant Got Vaporized

If you need evidence that Wall Street is a financial time bomb waiting for ignition look no further than the recent meltdown of Valeant Pharmaceuticals (VRX). In round terms, its market cap of $90 billion on August 5th has suddenly become the embodiment of that proverbial sucking sound to the south, having plunged by nearly two-thirds to only $34 billion by Friday’s close.

No, Valeant was not caught selling poison or torturing cats during the last 90 days. What is was doing for the past six years is aggressively pursuing every one of the financial engineering strategies that are worshipped and rewarded in the Wall Street casino.

Indeed, Valeant’s evolution during that period arose straight out of financial engineering central. That is, it was a creature of Goldman Sachs and the various dealers, underwriters, hedge funds and consulting firms which ply the Bubble Finance trade.

At the end of the day, the latter have turned the C-suites of corporate America into gambling dens by attracting, selecting and rewarding company wrecking speculators and debt-crazed buccaneers to the top corporate jobs.

In this case, the principal agent of destruction was a former M&A focussed McKinsey & Co consultant, Michael Pearson, who became CEO in 2008.

Pearson had apparently spent a career in the Dennis Kozlowski/Tyco school of corporate strategy. That is, advising clients to buy, not build; to slash staff and R&D spending, not invest; to set ridiculously ambitious “bigness” goals such as taking this tiny Canadian pharma specialist from its $800 million of sales to a goal of $20 billion practically overnight; to finance this 25X expansion with proceeds from Wall Street underwriters, not internally generated cash. He even replicated the Tyco strategy of moving the corporate HQ to Bermuda to slash its tax rate.

Pearson’s confederate in this scorched earth corporate “roll-up” enterprise was Howard Schiller, a 24-year veteran of Goldman Sachs, who became CFO in 2011, and soon completed the conversion of Valeant into a financial engineering machine.

During their tenure, Pearson and Schiller spent about $40 billion on some 150 acquisitions. And exactly what common expertise and value added leverage did these far flung acquisitions in contact lenses, ophthalmological therapies, dermatology, cosmeceuticals, anti-aging creams, Botox equivalents, acne fighters and much more bring to the table?

Well, what they brought was an opportunity to slash thousands of jobs, eliminate R&D, fund massive amounts of goodwill and intangible assets with cheap debt and, most especially, to fill Valeant’s purchase accounting cooking jars with fulsome amounts of reserves that can henceforth be used to cause inconvenient integration costs to disappear, as needed.

Indeed, Valeant not only failed to acquire any significant pharmacuetical synergies, but actually went in the opposite direction. That is, it has militantly eschewed investment in drug research and development in an industry who’s very purpose is the development of new drugs and therapies.

Yet the alternative strategy they peddled to the occupants of the hedge fund hotel that became increasingly crowded with VRX punters as its shares soared skyward was downright nonsensical and economically vapid. It could only have thrived during the late stages of a Bubble Finance mania.

In essence, Pearson and Schiller claimed that the rest of the industry was infinitely stupid, and that tens of billions of market cap could be created instantly by the simple expedient of buying companies with seasoned drugs and then jacking up prices, often by orders of magnitude.

In fact, Valeant has acquired a reputation for ferociously raising prices. In one year alone the company jacked-up the price of 81% of the drugs in its portfolio by an average of 66%.

The point here is not to echo the Hillary Chorus in favor of government drug price controls. Quite the contrary. Despite a crony capitalist inspired patent regime and the endless legal obstacles thrown up by the Big Pharma cartel, the drug market is not immune to the laws of economics.

Raise the price of drugs radically enough and you will attract competitors into the market with new formulations that circumvent the patent; or get greedy enough and generics will swamp you on the patent’s expiration.

Nor does that truth completely exempt even small volume or so-called orphan drugs. In those instances, it takes massive price gains to move the aggregate revenue needle. That is, exactly the kind of egregious increases that stir a political firestorm among users and providers and bring the Hillary brigade charging toward the TV cameras.

Accordingly, Martin Shkreli’s 5000% increase in the price of Daraprim went dark even faster than his company Twitter account.

Stated differently, what seasoned industry executives know that may have escaped the attention of 32-year Wall Street hot shots like Shkreli, or the spreadsheet jockeys who congregate in the hedge fund hotels, is that massive, wanton, overnight price escalation is not a business strategy that builds sustainable value and reinforces brand equity; it’s a scalping tactic that works in the casino, but not the real world.

At the same time, Pearson and Schiller slashed staff and chopped down R&D spending to a comically low 3% of sales. That compares to an industry norm of 12% to 18%.

Finally, this Wall Street witches brew was stirred together in pro forma financials that assumed these predatory price hikes would be permanent and that these back-of-the-envelope cost savings would be immediately realized in full.

The resulting profit projections, of course, had virtually nothing to do with the company’s actual results, but they did conform to sell-side hockey sticks like a hand-in-glove.

As the New York Times noted in an piece over the weekend:

Looking at Valeant’s real earnings compared with its make-believe ones exposes an enormous gulf. Under generally accepted accounting principles, the company earned $912.2 million in 2014. But Valeant’s preferred calculation showed “cash” earnings of $2.85 billion last year. That gap is far wider than at other pharmaceutical companies presenting adjusted figures.

Needless to say, it did not take long to turn Valeant into a veritable debt-mule. Its debt outstanding rose from $400 million in 2009 to $31 billion at present, and that’s the rub.

To wit, Valeant has been a veritable cash burning machine during its Wall Street driven M&A spree. So it has no possibility of making ends meet under a continuation of the maniacal M&A campaign crafted by the Wall Street wise guys.

Indeed, its demise is a near certainty. On the one hand, it was destined to blow-up if it kept “growing” via debt-fueled M&A. Contrariwise, its peak stock market value at 100X GAAP earnings was destined to implode if it stopped doing deals and triggered a mass exodus by the punters who inhabited VRX’s hedge fund hotel.

It goes without saying, of course, that these Bubble Finance deformations have resulted from the lunatic cheap money and wealth effects levitation policies of the Fed. Financial repression and QE deeply subsidize corporate borrowing to fund financial engineering deals, thereby reducing the after-tax cost of even sub-investment grade debt to low single digit levels.

Likewise, ZIRP is the mother’s milk of Wall Street speculation. It enables hedge funds and other fast money traders to build-up positions in rocket ships like Valeant at virtually no cost through the options and dealer financing markets.

Indeed, as VRX’s market cap grew from $14 billion to $90 billion in just 36 months, it generated a daisy chain of rising “collateral” value that enabled leveraged speculators to chase its stock to an ever more absurd height relative to the company’s GAAP financials.

During the 12 months ending in September, for example, VRX generated only $2.54 billion of operating cash flow, but spent $14.3 billion of cash on CapEx, M&A deals and other investments.

Nor was that an aberration. During the 27 quarters since the end of 2008, VRX has generated a mere $7 billion in operating cash flow, but has consumed nearly $26 billion of cash on investments and deals. Stated differently, it was a Wall Street Ponzi pure and simple.

Likewise, during that 27 quarter period, which roughly tracks Pearson’s tenure, the company has posted rapidly rising sales—-with the top line growing from $757 million in 2008 to $10 billion in its most recent LTM report.

But it has been an absolutely profitless prosperity—–not unlike the typical financial engineering driven roll-up. Thus, over this 27 quarter period as a whole, sales totaled just under $30 billion, but its cumulative net income amounted to a miniscule $130 million.

That’s right. Over the last seven years, Valeant’s GAAP profits have amounted to just 0.4% of sales.

So why did Valeant’s market cap soar from $1.2 billion, when Pearson arrived in 2008, to the recent peak of $90 billion during a period when the company has generated hardly a dime of profits?

It was just another case of Wall Street financial engineering and speculative hype at work. The entire story has been based on pro forma, ex-items forward looking Wall Street hockey sticks, and not the least those published by Goldman Sachs.

Yet there is no mystery as to why these financial engineering scams happen over and again in financial markets which have been corrupted and disabled by the Fed and other central banks.

Namely, because the deal fees from financial engineering are so lucrative; and because the checks and balance of a healthy free market in finance——such as short-sellers, heavy hedging expense and meaningful carry costs for debt financed speculations—–have been destroyed by the central banks.

Thus, a few years ago Valeant’s predecessor company was a backwater player on the Toronto stock exchange, but in the last three years it has become the fifth largest payer of investment banker fees on Wall Street.

In fact, thanks to its rapid acquisition-driven and debt-financed expansion Valeant’s investment banking fees have totaled $500 million since 2012. This means that only General Electric Co, Allergan Plc., AT&T Inc. and Dell Inc have paid more, according to data from Freeman and Co.

Needless to say, financial engineering scams like Tyco and Valeant would never happen in an honest free market. Short sellers would shut them down long before they reach egregious levels of over-valuation; and the cost of honest downside market insurance (i.e. S&P 500 puts) and market driven carry cost would dramatically reduce the profitability of speculation and the amount of punters and capital in the casino.

In today’s broken markets and corrupt regime of central bank driven crony capitalism, however, bubbles inflate in individual securities, as well as in broad sectors (e.g. biotech, social media and junk bonds) and the market as a whole, until they reach egregious, self-correcting extremes. Then they violently implode, creating immense waves of collateral damage in the process.

Recall that Tyco’s market cap dropped from $125 billion to $25 billion during just the final six months before Kozlowski was finally forced out in June 2002. Likewise, during the last 90 days nearly $250 billion has evaporated from the 150 companies in the NADAQ biotech index.

Viewed in the larger context, therefore, Valeant’s $55 billion implosion in recent weeks is just a preliminary tremor. On a worldwide basis, the mother of all financial bubbles is just beginning to fracture.

Accordingly, in the US alone there is probably another $15 trillion of bottled air waiting to be released. Perhaps then the American people will learn that Yellen & Co have actually been in the un-wealth effects business for way too long.

Subscribe to:

Comments (Atom)